Why Early Oncology Launches Often Look “Too Good” in the Sales Data

Early oncology launches often look unusually strong because the data is incomplete. Let's find out what is happening.

Sanju Rajan

1/4/20263 min read

TL;DR: Early oncology launches often look unusually strong because early sales data reflect total WAC dollars before rebates, discounts, and access controls fully take effect. That picture is incomplete, so if you’re forecasting your own launch or benchmarking against competitor analogs, don’t assume early performance is permanent.

Imagine you are preparing to launch a new oncology drug. You want to set expectations internally, so you start by looking at how similar drugs performed at launch. You pull sales data on a few recent oncology launches. The early numbers look strong. Revenue seems to track closely with list-price sales. Discounts appear small. Access looks relatively smooth.

At first glance, this is encouraging. It can feel like proof that oncology launches face limited pricing pressure and that strong early performance is achievable. Before drawing that conclusion, it is important to understand what those early numbers are actually showing.

What You Are Really Seeing in Early Launch Data

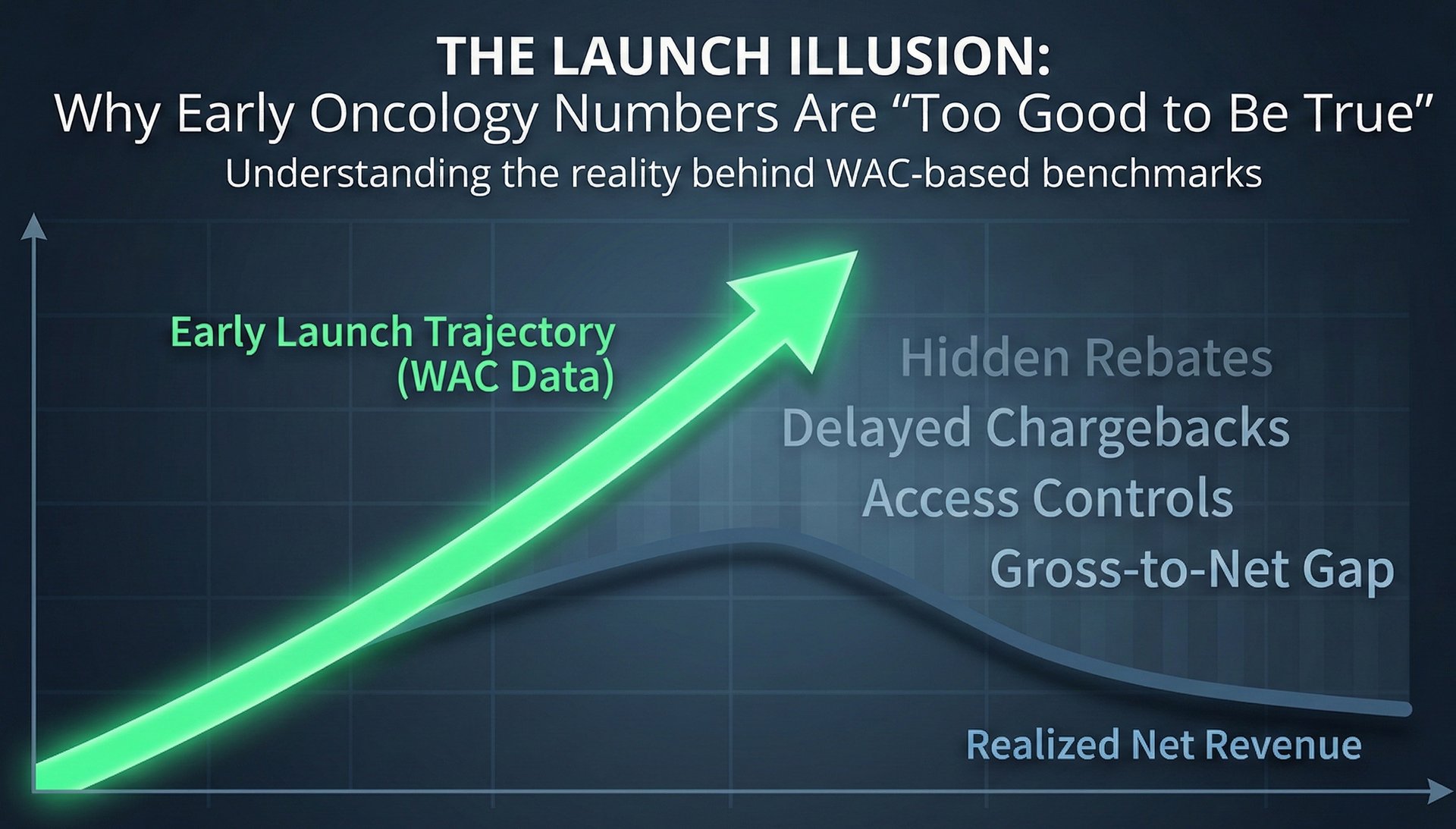

Most early-launch benchmarks are based on WAC-based sales. WAC, or Wholesale Acquisition Cost, is the manufacturer’s list price. Many commercial datasets report WAC multiplied by the number of units shipped or dispensed.

These numbers show how much product moved at the list price. They do not show how much money the manufacturer ultimately keeps.

Early in a launch, there has been little time for rebates, discounts, and fees to be applied and recognized. Government exposure is still low. Chargebacks and returns often appear later. Because of this timing, WAC-based sales and reported revenue tend to sit close together in the first few months.

This makes early launches look cleaner and more profitable than they will appear later.

Why Discounts and Rebates Look Small at the Beginning

Gross-to-net represents the share of the list price that is given up through rebates, discounts, and fees. In oncology, gross-to-net is typically low in the early quarters of a launch.

There are several reasons for this. Patient populations are small and clearly defined. Payers have limited leverage early on. Contracting pressure builds only after real utilization is visible. Many rebates are calculated and recognized after sales occur, not at the point of sale.

The financial impact of these concessions is expected from the start. It simply does not appear in the data immediately.

How ASP Can Reinforce the Illusion

When reviewing early benchmarks, you may also consider ASP. Average Sales Price is a Medicare reimbursement metric. It reflects some discounts but not all, and it is reported with a delay.

Early in a launch, ASP often sits close to WAC. This can reinforce the impression that pricing is strong or that discounts are minimal. ASP is helpful for understanding provider reimbursement, especially in buy-and-bill settings. It should not be used to estimate manufacturer revenue or overall commercial performance.

Why Early Access Looks Easier Than It Really Is

Early access patterns can also look favorable. Coverage policies are still being written. Utilization management is limited. Many payers allow access while they observe real-world use.

This early period can appear to signal broad acceptance. Over time, as patient volume grows and budget impact becomes clearer, controls tend to increase. Prior authorization requirements, step edits, and contracting pressure often follow.

Early access reflects a temporary lack of restrictions, not a final access outcome.

As months pass, the picture becomes more realistic. Medicare and Medicaid exposure grows. 340B share increases. Rebates deepen. Competition enters the market. Gross-to-net expands.

Revenue begins to separate from WAC-based sales. This does not mean the product is underperforming. It means the market has moved from launch mode to steady-state behavior.

How to Use Early Launch Benchmarks Correctly

When comparing your upcoming launch to prior oncology analogs, early data should be used carefully. It is best suited for understanding demand, diagnosis rates, and early execution.

It is not a reliable guide to long-term net pricing or steady-state revenue.

Strong early numbers are common in oncology. They do not guarantee sustained economics.

Closing Thoughts

Early oncology launches often look “too good” because discounts, rebates, and access controls have not yet fully materialized. The data is incomplete. Understanding this context helps set realistic expectations and avoids drawing the wrong conclusions when planning a launch or evaluating competitors.